Abstract

Forecasting the exchange rates is both a challenging and important task for the modern traders, people working in the financial markets and general population across the globe. In this paper we will be utilizing the time series concepts to do an analysis and predict the daily exchange rates of the Indian Rupee (INR) against the United States Dollar (USD). This paper will investigate and compare different forecasting techniques like ARIMA, Holt-Winters simple exponential smoothing and Neural networks. Further, utilizing the above techniques investigate the behavior of daily exchange rates of the Indian Rupee (INR) against the United States Dollar. Daily exchange rates from 19th November 2007 to 18th December 2017 were used for the analysis.

View Paper:

Overview

This study focuses on forecasting the USD to INR exchange rate using time series analysis. The research compares different forecasting techniques, including Holt-Winters Simple Exponential Smoothing, ARIMA, and Neural Networks, to evaluate their predictive accuracy. The dataset consists of 10 years of historical exchange rate data, and the study aims to identify the most effective method for short-term exchange rate predictions.

Methodology

The research employs time series modeling techniques to analyze historical exchange rates.

- Explores traditional economic models like Purchasing Power Parity (PPP) and Relative Economic Strength before applying statistical methods such as ARIMA and Holt-Winters smoothing.

- Neural Network Autoregression (NNAR) model is implemented for comparative analysis. The models are evaluated based on accuracy metrics like Mean Absolute Percentage Error (MAPE).

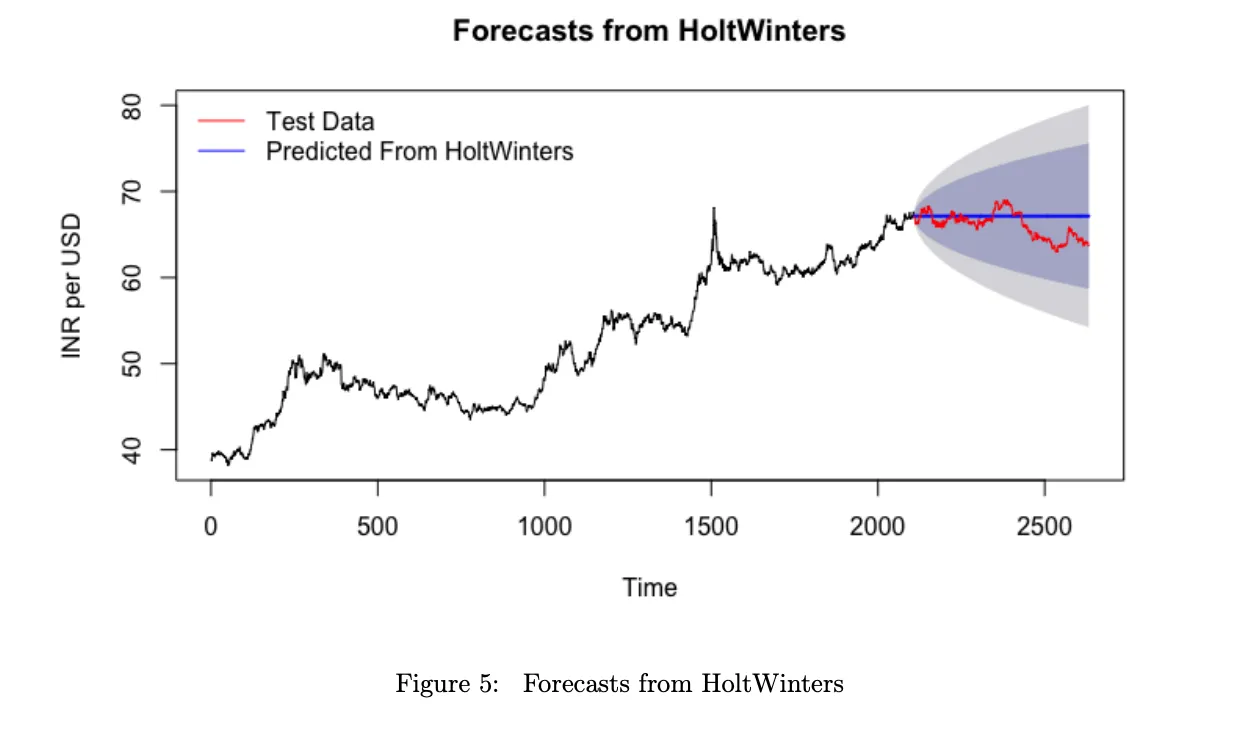

Forecasts from HoltWinters

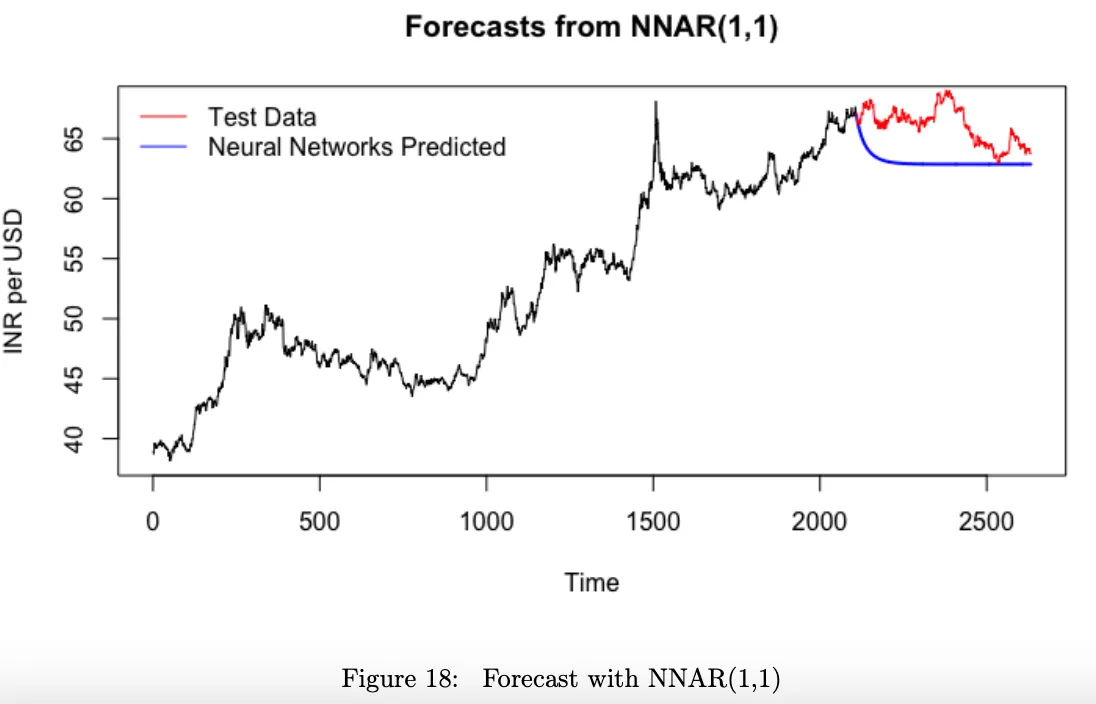

Forecasts from NNAR

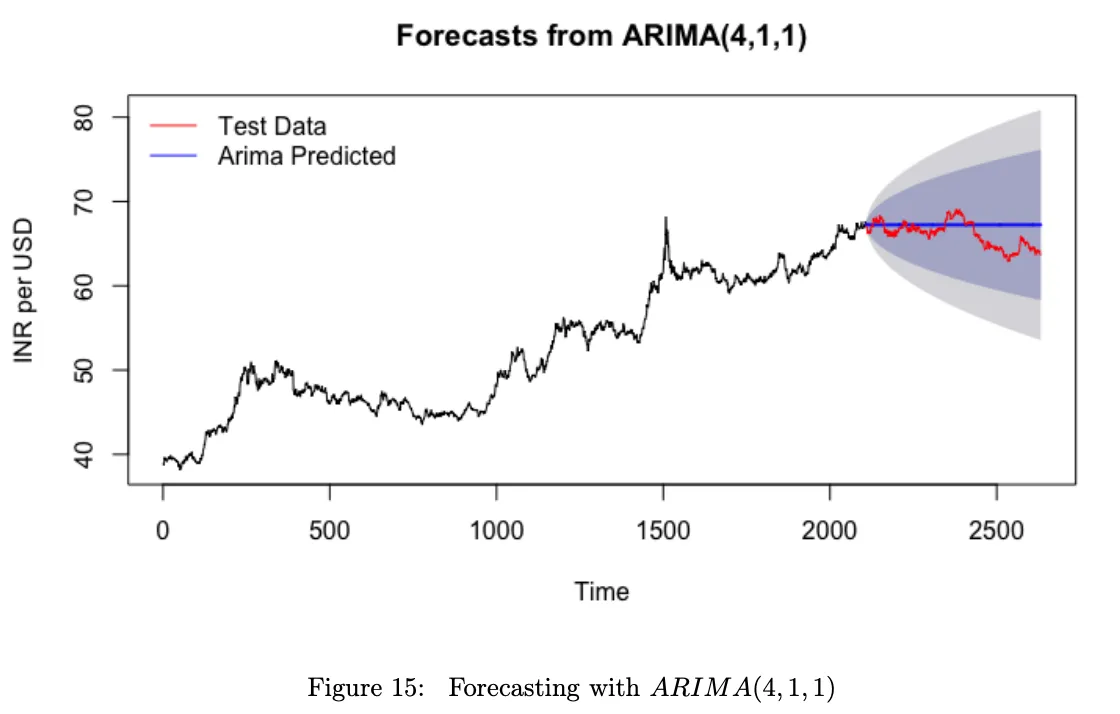

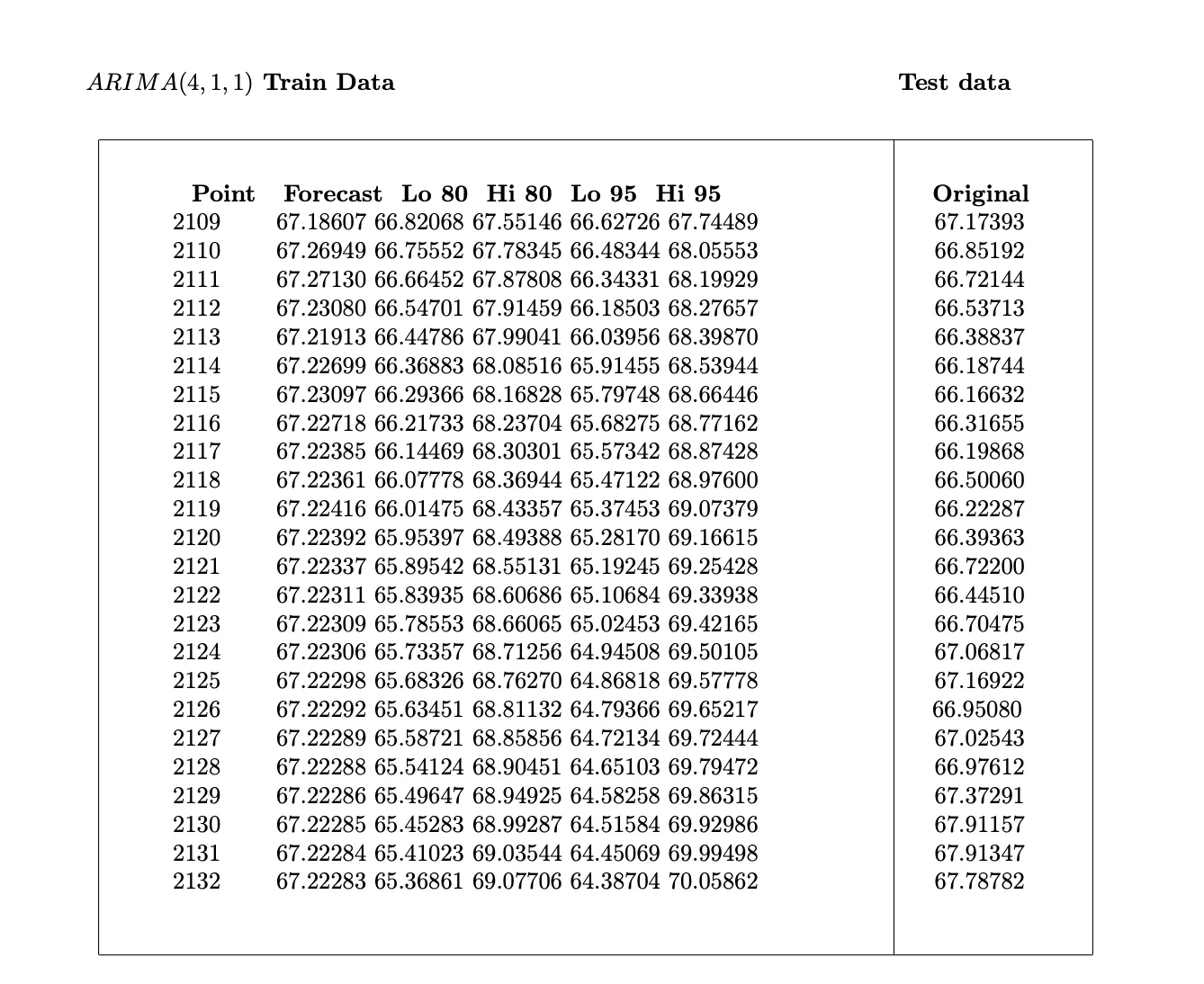

Forecasts from ARIMA

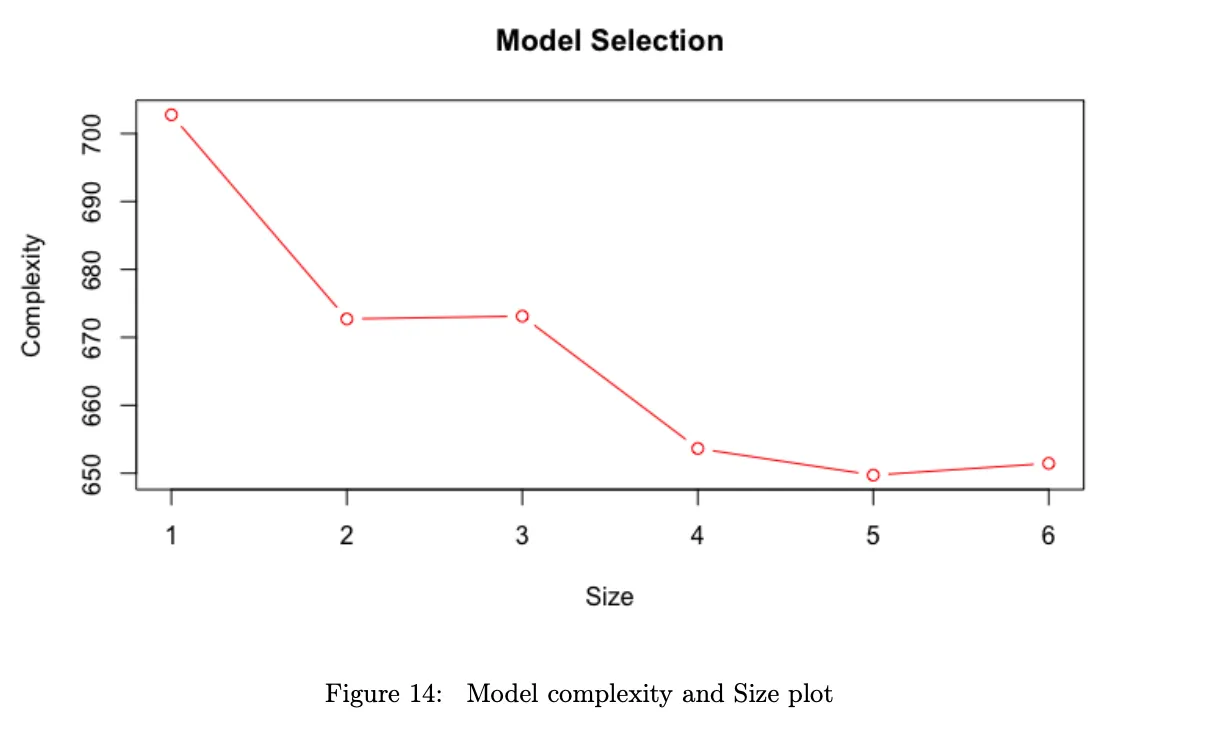

Model Selection

Output

Technologies

R, Time-Series Analysis, ARIMA, HoltWinters, Auto-Regressive, Moving-Averages, Exponential Smoothing, NNAR, Exponential Smoothing